Ok, well I’m a sucker for a problem, so here goes.

X = np.linspace(1, 276, 276)

X = X.astype(int)

df = pd.read_csv('Datapy.csv')

with pm.Model() as model:

# Priors

alpha =pm.Normal('alpha', 20, 5)

#alpha = alpha.astype(int)

beta = pm.Normal('beta', 0, 1)

#beta = beta.astype(int)

gam = pm.Normal('gam', mu=0.0, sigma=0.1)

#gam = gam.astype(int)

σ = pm.HalfNormal("σ", sigma=10)

ξ = pm.Normal("ξ", mu=0.0, sigma=0.1)

# Expected value of outcome

#μ = pm.Normal("μ", mu=20, sigma=5)

μ = alpha + beta*X + gam*X**2

# Estimation

gev = pmx.GenExtreme("gev", mu=μ, sigma=σ, xi=ξ, observed=df.r)

idata = pm.sample_prior_predictive(samples=1000, model=model)

az.plot_ppc(idata, group="prior", figsize=(8, 3))

ax = plt.gca()

ax = plt.gca()

ax.set_xlim([-50, 200])

ax.set_ylim([0, 0.04]);

az.plot_posterior(idata, group="prior", var_names=["alpha","beta","gam","σ","ξ"], hdi_prob="hide", point_estimate=None, figsize=(8, 3));

with model:

trace = pm.sample(

500,

cores=4,

chains=4,

tune=2000,

initvals={'alpha':22, 'beta': -0.01, "gam": 0.0, "σ": 15.0, "ξ": 0.2},

#initvals={'alpha':0.92, 'beta': -2.5, "gam": 0.9, "μ": 50, "σ": 3.0, "ξ": -0.1},

target_accept=0.9,

)

idata.extend(trace)

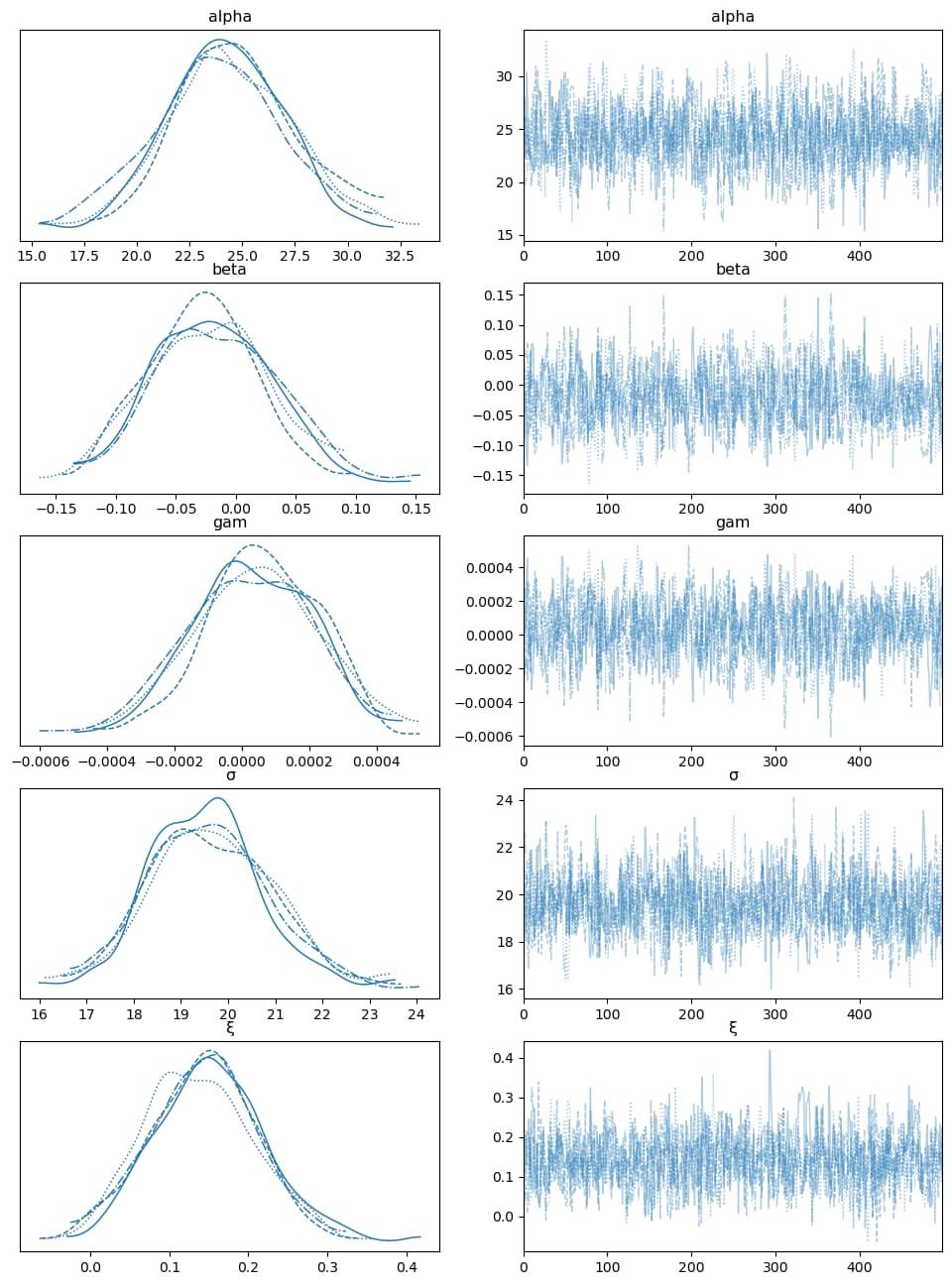

az.plot_trace(idata, var_names=["alpha", "beta", "gam", "σ", "ξ"], figsize=(12, 16));

The main thing was to choose more reasonable priors. Building up from a single GEV distribution fit showed that the X wasn’t so influential: beta is small and gam is close to zero. Also, the target value should be < 1.0 and it’s good to let the sampler select its own starting point, at least initially.

Compare the prior predictive check for the case for no linear dependence with the one for the quadratic dependence with these much tigher priors. It gives a good idea how important priors are here.

No linear dependence (7 secs)

Samples great.

Linear dependence (8 secs)

Needs a sensible prior for alpha and beta.

Quadratic dependence (37 secs)

Samples badly - can be lots of divergences, even with tight priors for gam, reasonable initvals and a higher target_accept.

With integers

Turning even just alpha to an astype(int) causes the sampling to go nuts (haha!) - it takes about 450 seconds then and looks just awful. DO you really need these parameters to be ints?