I have a dataset that describes the wealth index of Rwandan housholds: wealth.csv (29.0 KB)

Its shape and distribution is:

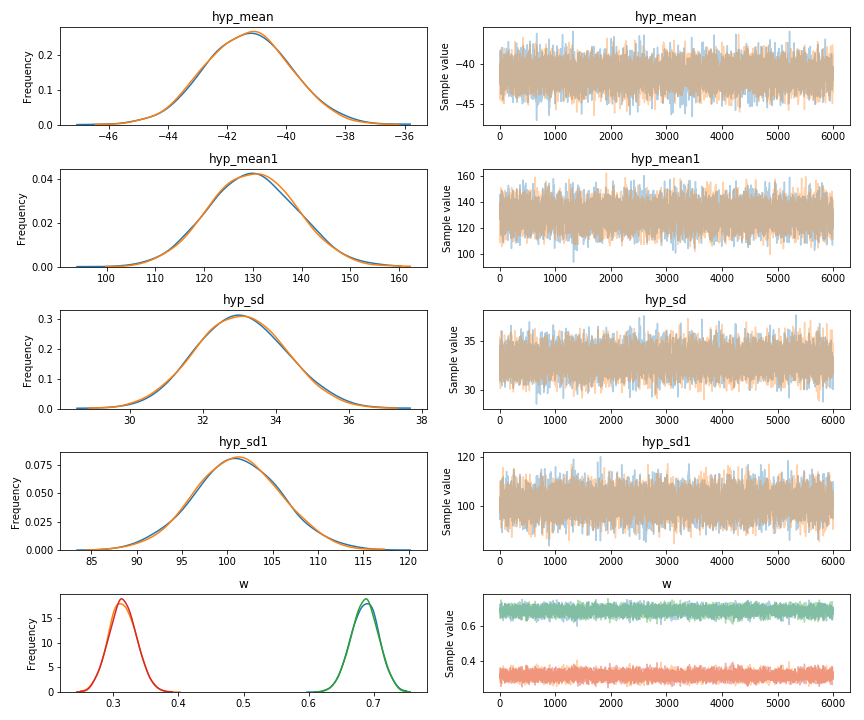

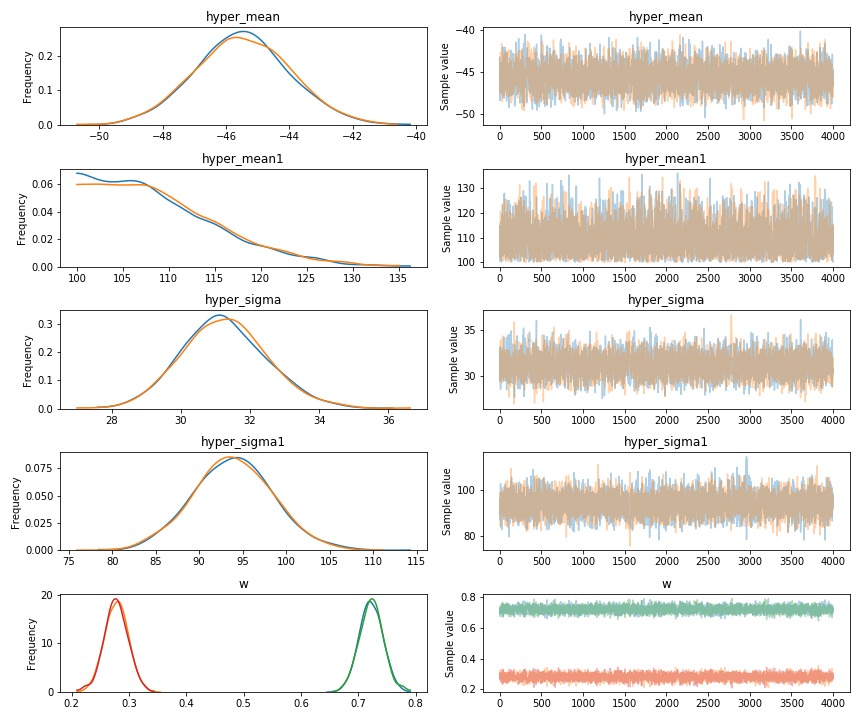

I am using Pymc3 Mixture Modeling to divide wealth index into 2 separate groups (presumably rich and poor).

with pm.Model() as model:

hyper_mean = pm.Uniform('hyper_mean', -100, 10)

hyper_mean1 = pm.Uniform('hyper_mean1', 100, 300)

hyper_sigma = pm.Uniform('hyper_sigma', 0, 100)

hyper_sigma1 = pm.Uniform('hyper_sigma1', 0, 150)

component = pm.Normal.dist(mu=hyper_mean, sd=hyper_sigma)

component1 = pm.Normal.dist(mu=hyper_mean1, sd=hyper_sigma1)

w = pm.Dirichlet('w', a=np.array([1, 1]))

like = pm.Mixture('like', w=w, comp_dists=[component, component1], observed=data)

with model:

trace = pm.sample(5000, tune=2500, njobs=1)[1000:]

As I am uncertain about the prior parameters of Rwandan wealth, I (think I) am using non restrictive priors; thus allowing the data to have a strong influence on the posterior.

Resulting in:

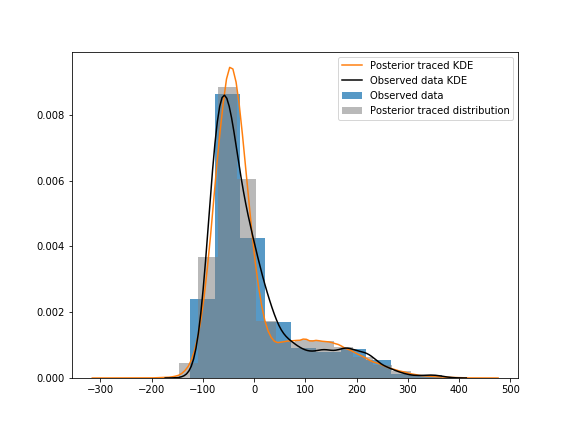

When I visualize posterior values over observed data, the observed data is flatter around the 100-200 wealth index:

I’ve tried using the Student_T distribution as the components instead of the Normal one, but it gave the model longer tails and a bigger hump around the 100-200 mark.

With the priors being so non restrictive, I would think the data would take over the posterior.

Do you suggest using a different distribution to represent the components, or reparametrize, or do anything else to have the posterior align better?