Hi evertone from the comunity.

I am a beginner on data analysis in general and I have this project to do and I hope someone could give me some advice.

The project consists of modelling counting data with a Poisson regression model and make point estimate the paramaters of the model using Metropolis-Hastings algorithm using pymc3 library.

The dataset that I have to use is a very simple one. It’s about observations of Insurance Motor Third Party Claims (both frequenct and severity). I’ll link the full description of the dataset below.

https://search.r-project.org/CRAN/refmans/GLMsData/html/motorins.html

There are two issues that I am dealing with:

-

Do I have to do some preprocessing step before running the algorithm? If so, how do I do it?

-

I built a model following the Poisson regression model in the example section, but still the the algorithm is too slow. How I can improve performance?

Here is the code I used until now:

import arviz as az

import bambi as bmb

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

import pymc3 as pm

import seaborn as sns

import theano

import theano.tensor as tt

import xarray as xr

from formulae import design_matrices

print(f"Running on PyMC3 v{pm.__version__}")

print(f"Running on Arviz v{az.__version__}")

df = pd.read_csv('SwedishMotorInsurance.csv')

df.head()

df['Rate']=df['Claims']/df['Insured']

fml = "linear ~ Kilometres + Zone + Bonus + Make"

df_1=df[['linear','Kilometres','Zone','Bonus','Make']]

dm = design_matrices(fml, df_1, na_action="error")

mx_ex = dm.common.as_dataframe()

mx_en = dm.response.as_dataframe()

with pm.Model() as model:

# define priors, weakly informative Normal

b0 = pm.Normal("Intercept", mu=0, sigma=10)

b1 = pm.Normal("Kilometres", mu=0, sigma=10)

b2 = pm.Normal("Zone", mu=0, sigma=10)

b3 = pm.Normal("Bonus", mu=0, sigma=10)

b4 = pm.Normal("Make", mu=0, sigma=10)

# define linear model and exp link function

theta = (

b0

+ b1 * mx_ex["Kilometres"].values

+ b2 * mx_ex["Zone"].values

+ b3 * mx_ex["Bonus"].values

+ b4 * mx_ex["Make"].values

)

## Define Poisson likelihood

y = pm.Poisson("y", mu=tt.exp(theta), observed=mx_en["linear"].values)

with model:

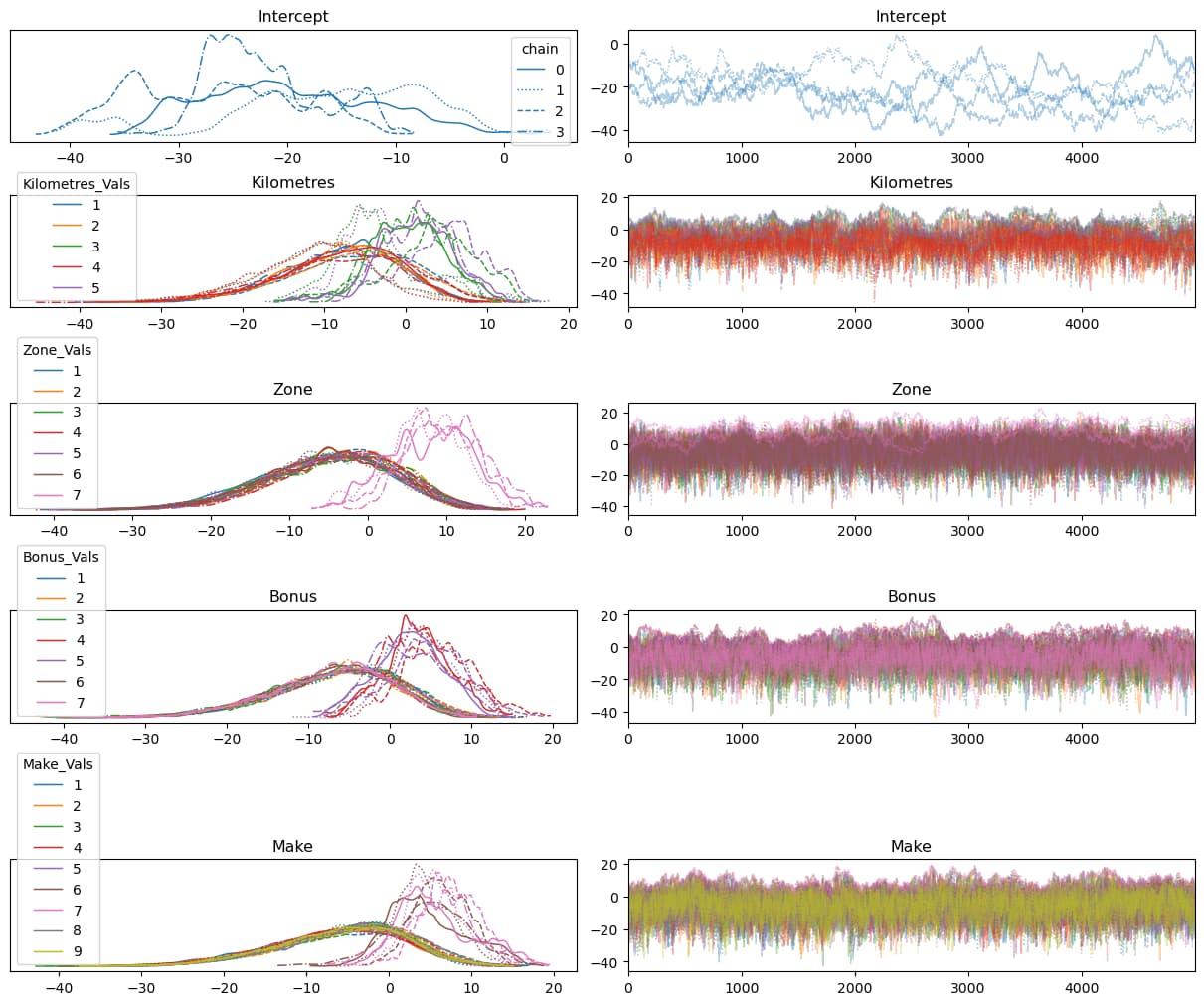

trace = pm.sample(draws=5000, tune=500, cores=4, random_seed=45, step=pm.Metropolis())

pm.summary(trace)

How would you modify it?

Here is the dataset file.

SwedishMotorInsurance.csv (49.6 KB)

Hope this would be useful for other beginners like me.